The first time I added up my own net worth, I left my pension out completely. It felt like cheating to count money I couldn’t touch for another twenty-odd years. The figure I landed on looked tidy and honest. It was also wrong by a wide margin, because the single biggest asset I owned was sitting in a workplace pension I’d decided didn’t count.

That instinct is incredibly common, and it’s almost exactly backwards. With a house, people argue about whether to include something they can see and live in. With a pension, they drop the largest number on the page because it lives behind a locked door. Both habits distort the picture. This is the pension half of the question, and it has a couple of twists the house never has.

Here’s the short version. A pension is an asset you own, so it belongs in your net worth. The genuinely tricky parts are which pensions get a clean number and which don’t, and why the State Pension sits in a different category altogether.

Verdly publishes for education, not financial advice; speak to a regulated adviser for decisions specific to your situation.

Net worth and “money I can spend” are two different questions

The reason people leave pensions out usually isn’t a considered accounting choice. It’s a feeling: I can’t get at it, so it doesn’t feel like mine yet. Under current rules you generally can’t access a private pension until your late fifties, and that minimum age is set to rise from 55 to 57 in 2028. So for anyone in their twenties, thirties or forties, the pension is real money they can’t lay a finger on for years.

But net worth was never a measure of what you can spend this afternoon. It’s a snapshot of what you own minus what you owe. Accessibility is a separate axis entirely. Your emergency fund and your pension can hold the same number and play completely different roles: one is reachable today, the other compounding out of reach until a birthday years away. Leaving the pension out doesn’t make your finances more honest. It just hides the part of them that’s doing the most work.

Defined contribution: the easy case

Most people paying into a workplace or personal pension today have a defined contribution (DC) pension. You, and usually your employer, pay in; the money is invested; the pot is worth whatever it’s worth on a given day. Auto-enrolment means a large share of UK employees now have one of these whether they think about it or not.

Valuing it is the simplest job on your whole balance sheet. Log in, read the current pot value, write it down. That’s it. A DC pot is an owned asset with a live market value, no different in principle from a Stocks and Shares ISA. There’s no clever adjustment to make and no reason to discount it for being locked away, because illiquidity changes what you can do with an asset, not what it’s worth.

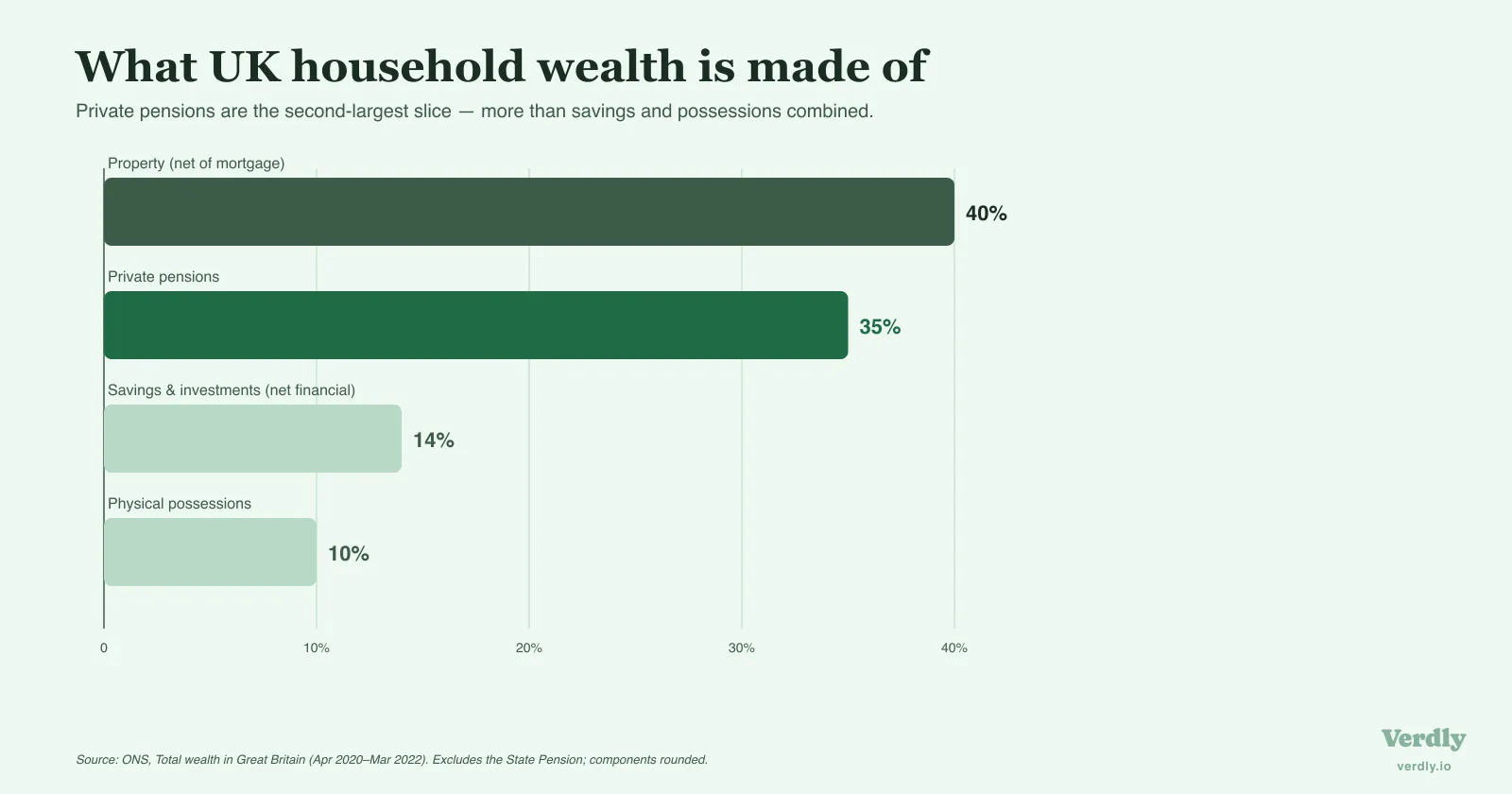

It matters more than it might sound, because for many households the pension is not a minor line. According to the ONS figures for April 2020 to March 2022, private pensions made up around 35% of all household wealth in Great Britain, second only to property at 40% and far ahead of financial wealth like savings and investments at 14%. Drop the pension from your own sums and, for a typical saver, you’re rubbing out roughly a third of the picture.

Defined benefit: the number that won’t sit still

Defined benefit (DB) pensions, the old final-salary and career-average schemes still common in the public sector, are where the tidy answer falls apart. A DB pension doesn’t have a pot. It’s a promise: a certain income each year for the rest of your life once you retire, usually rising with inflation. There’s no balance to read off a screen, which is exactly why so many people leave these out by default.

You can still put a value on it, but you’re estimating rather than reading. The honest way to think about a DB pension is to ask what lump sum it would take to buy that guaranteed, inflation-linked income on the open market, which is a much larger figure than people expect. The ONS values DB pension wealth by capitalising that future income stream, and a rough shorthand sometimes used is to treat the pension as worth around twenty times the annual income it promises. A DB pension paying £10,000 a year, on that shorthand, represents something like £200,000 of wealth.

Two caveats sit right next to that number. First, the multiple is a blunt rule of thumb, not a market price; the real cost of buying that income shifts with interest rates and your age, and your scheme’s own transfer value can differ a lot. Treat any figure you use as an estimate carrying a wide margin, not a precise asset value. (And a transfer value is a valuation tool here, not a nudge to do anything with the pension.) Second, even the official statistics are contested: the Institute for Fiscal Studies has shown that changing the valuation method moves measured pension wealth by enormous amounts, which is part of why the ONS survey itself had its national-statistics badge withdrawn in 2025. If the experts can’t pin DB wealth to a single figure, you don’t need to either. Pick a sensible method, write down which one you used, and stay consistent so the trend means something.

The State Pension is the exception

Here’s the part that trips people up most. The State Pension is not part of your net worth, and that isn’t an oversight.

Net worth counts assets you own: things with a value you could, in principle, sell or transfer. The State Pension is neither. It’s an entitlement built from your National Insurance record, a promise of future income from the government rather than a pot with your name on it. You can’t sell it, you can’t pass it on, and it has no transfer value. It behaves like a future salary, not like savings. So it stays out of the net worth column, the same way the wages you’ll earn next year stay out.

That’s not the same as saying it doesn’t matter. The State Pension is one of the most valuable income streams most people will ever have, and it does real work in a retirement plan by reducing how much your own savings need to cover. It just does that work as income, not as an asset on today’s balance sheet. Keeping it out keeps the two ideas from blurring into one.

What it looks like with real numbers

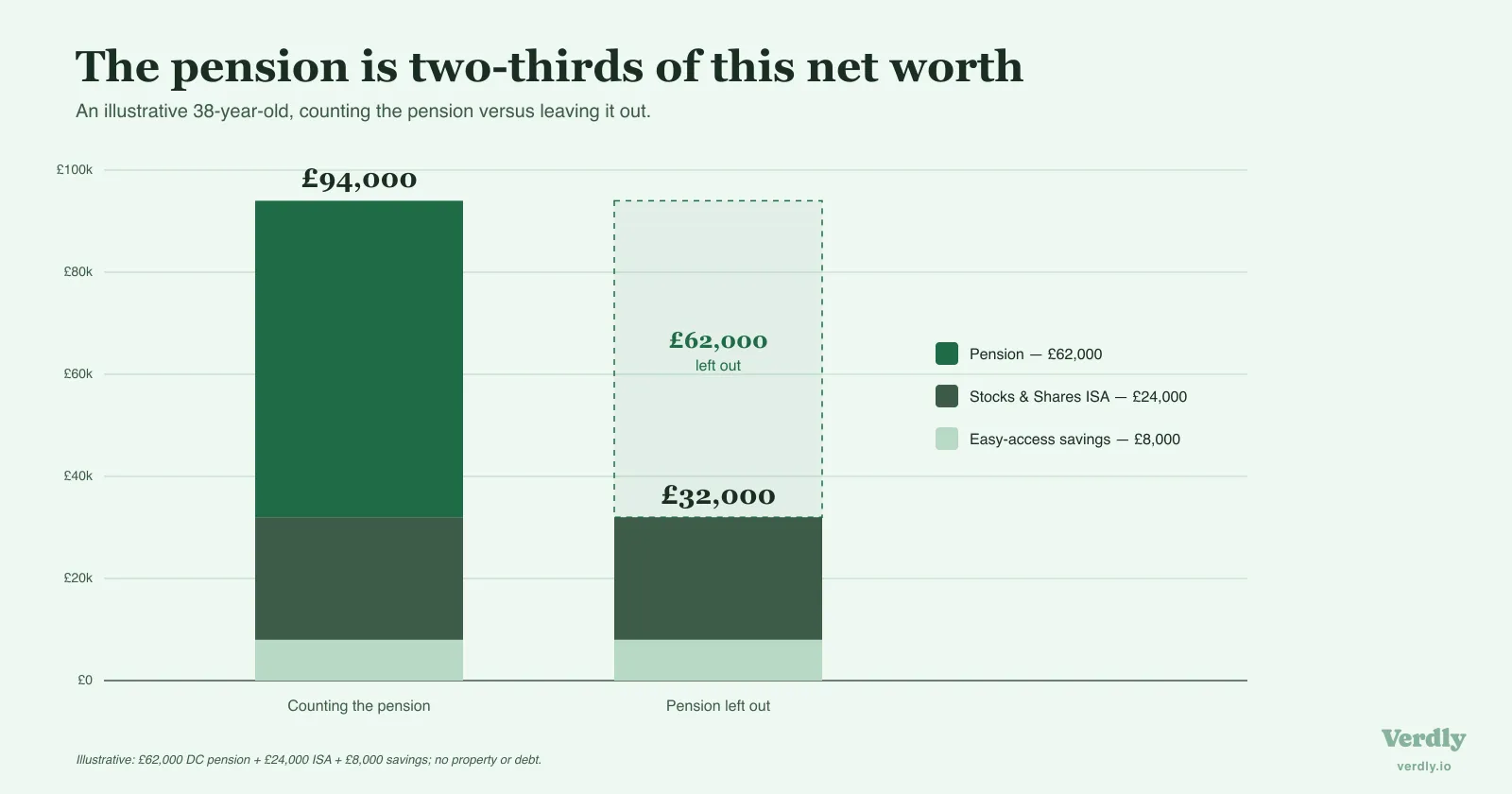

Take someone at 38, renting, with a workplace pension they’ve barely glanced at. The DC pot holds £62,000. Alongside it sits £24,000 in a Stocks and Shares ISA and £8,000 in easy-access savings. No property, no debt.

Their net worth is £94,000. Of that, the pension alone is £62,000: roughly two-thirds of everything they own. Now run the instinct from the top of this piece. Leave the pension out because it’s locked away, and the same person looks like they’re worth £32,000. Same accounts, same life, and a number that’s understated by nearly two-thirds.

Both framings come from the same person. One of them is their actual financial position. The other is what they can reach this month. That second figure is worth knowing too, but it’s the answer to a different question, and swapping one for the other is how people end up badly misjudging where they stand. If you want to see how a number like this sits against the wider population, it’s worth knowing that the UK averages by age include pension wealth as standard, so a like-for-like comparison has to keep the pension in.

Keeping the pension where it belongs

A pension is the rare asset people are tempted to undercount, not inflate. It’s locked away, it doesn’t show up in your banking app, and a DB version doesn’t even hand you a number to copy down. All of which makes it easy to leave off, and leaving it off is how the biggest thing you own becomes invisible to you.

The fix is unglamorous. Count the DC pots at their current value, put a sensible and clearly-labelled estimate on any DB pension, and keep the State Pension out as the future income it is. Then watch the whole thing over time rather than in a single nervous sitting, because a pension’s value is a story told across decades, not a figure you check once. That’s the case for giving it a permanent line of its own and logging your pension alongside your other assets, so the largest, slowest-moving part of your wealth stops hiding behind a door you can’t open yet. The home was the asset where the include-or-exclude question ran hottest. The pension is the one where the honest answer is simply to stop pretending it isn’t there.

Last reviewed 29 June 2026.