Ask an American money forum whether your student loan counts against your net worth and the answer comes back in one word: yes. It’s a debt, you subtract it, next question. Ask the same thing on a British forum and you get a two-hundred-comment argument, because a UK student loan is a strange kind of debt that behaves almost nothing like the American version people are picturing.

The disagreement is real, and both camps have a point. One says a balance you owe is a liability, full stop, so it comes off your assets like any other debt. The other says a loan you might never fully repay, that vanishes after a set number of years and never shows up on your credit file, isn’t really a debt in the way a car loan is. Getting this right matters most for the people carrying the biggest balances: recent graduates, for whom the loan can be the largest single number on an otherwise thin balance sheet.

Here’s the short answer, then the part worth understanding. In the strict accounting sense, yes: your outstanding balance is a liability, and net worth is what you own minus what you owe, so it comes off the total. The more useful question is what that number actually tells you, because a UK student loan can sit on your balance sheet looking far more threatening than it will ever turn out to be.

Verdly publishes for education, not financial advice; speak to a regulated adviser for decisions specific to your situation.

Net worth doesn’t care what the debt is called

Net worth is a blunt instrument, and that’s its strength. Add up everything you own, subtract everything you owe, and the figure left over is where you stand. It doesn’t weigh a mortgage differently from an overdraft, or ask whether a debt is “good” or “bad”. A liability is a liability. On that definition your student loan balance belongs in the “owe” column, and leaving it out simply flatters the number.

So if you want a single, consistent, comparable figure, count it. The complication isn’t whether it belongs. It’s that the headline balance and the amount you’ll really hand over can be two very different numbers.

Why a UK student loan isn’t like other debt

Almost everything that makes a debt feel like a debt is missing here. You don’t repay a UK student loan on a fixed schedule tied to what you borrowed. You repay 9% of everything you earn above a threshold that depends on your plan, and nothing at all below it. Lose your job and the repayments stop on their own. Get a pay rise and they climb. Postgraduate loans work the same way at 6%. That isn’t how a bank loan behaves. It’s how a tax behaves.

Two more features push it further from ordinary debt. It doesn’t appear on your credit file, so it can’t drag down a credit score the way a maxed-out card can, though a mortgage lender will still factor the monthly repayment into the income they’ll lend against. And it doesn’t last forever. Every plan has a write-off date, after which whatever is left simply disappears, cancelled with no consequences and no mark on anything. A debt with an expiry date is a genuinely odd thing to carry on a balance sheet.

The balance is a worst case, not a forecast

This is where the American “just subtract it” rule starts to mislead. For a great many graduates, the full balance is a number they will never pay. Because repayments track income and the clock eventually runs out, the loan is written off before it’s cleared for anyone whose earnings never climb high enough to catch up with the interest.

And that isn’t a rare edge case. The Institute for Fiscal Studies estimates that only around half of students starting under the current system will repay in full, and under the older Plan 2 terms the share expected to clear the whole thing was lower still. For everyone else, the balance on the statement is a ceiling, not a bill. It sets the most you could pay, while what you’ll actually pay is decided by your future earnings and the write-off clock, not by the number itself.

That’s why the loan can look so alarming and cost so little. A graduate can enter repayment owing north of £45,000 and, on a middling career income, repay a steady slice of salary for decades without the balance ever reaching zero before it’s wiped. The headline figure never described their real cost.

Which plan you’re on changes the picture

“Student loan” isn’t one thing, and the differences matter for how seriously to take the balance.

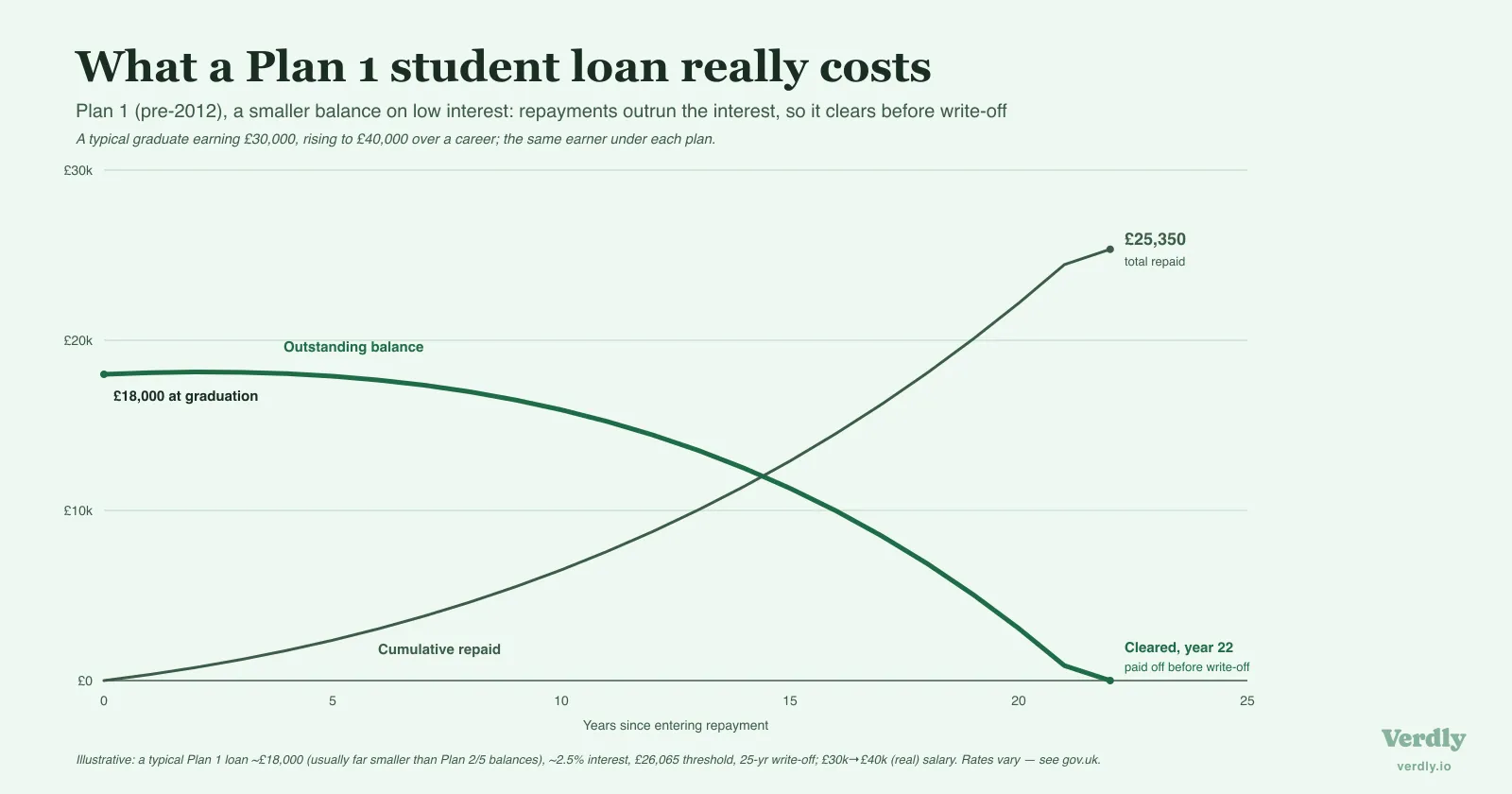

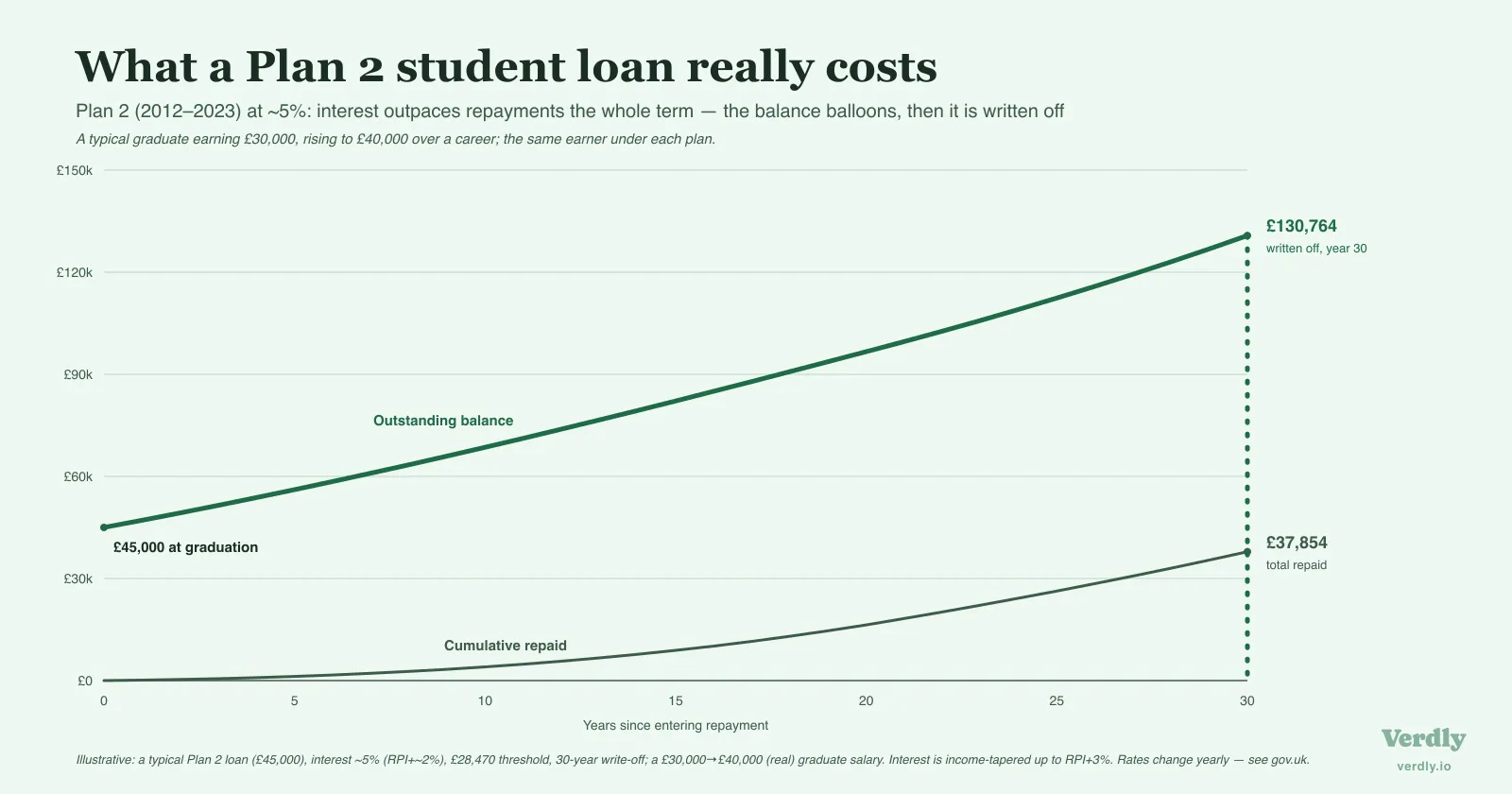

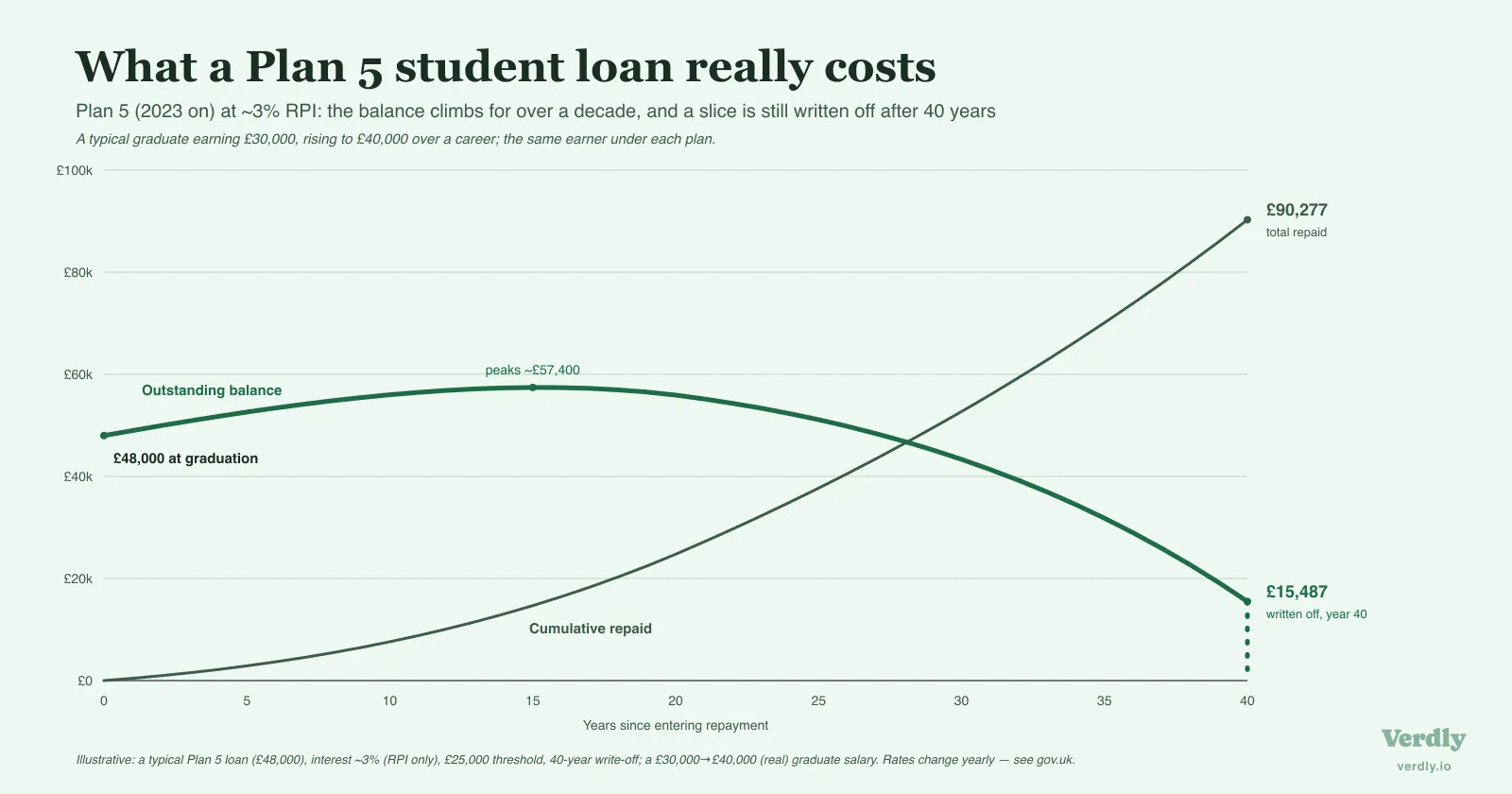

Plan 2, which covers most English and Welsh students who started between 2012 and 2023, charges interest of RPI plus up to 3% and is written off 30 years after you were first due to repay. Plan 5, for English students who started from September 2023, charges RPI only, so the balance doesn’t grow in real terms, but it runs for 40 years before write-off. Plan 1 and Plan 4 in Scotland have their own thresholds and a 25 to 30-year write-off. Postgraduate loans stack on top at their own rate.

The practical upshot: a Plan 2 balance ballooning under high interest can look terrifying while staying largely theoretical for a modest earner, whereas a Plan 5 balance grows more slowly but hangs around a decade longer. If you’re going to record the number, it’s worth knowing which of these you actually hold, because the same £45,000 means something different under each.

The charts below follow one typical graduate, on pay starting at £30,000 and climbing to £40,000, through each plan in turn, so the differences you see are the plan’s doing rather than the borrower’s.

So what do you actually write down?

Count the balance. It’s the honest, consistent figure, and it keeps your net worth comparable with everyone else’s and with the UK averages by age, which treat the loan as a straightforward liability. But hold a second thought next to it, much as you would with a home you can’t spend or a pension you can’t yet reach: the balance is the pessimistic version of your finances, not the likely one.

That second thought is where the “should I overpay?” question comes from, and it’s worth being clear-eyed rather than prescriptive about it. Overpaying a student loan only saves you money if you’d otherwise have repaid the whole thing before write-off. For the roughly half of borrowers who won’t, voluntary payments hand over cash that was going to be cancelled anyway. For a high earner on course to clear it early, the sums look different. Which of those describes you turns on your future income, which nobody knows in advance, and that uncertainty is the whole point: the balance is a fact, but its weight isn’t.

What it looks like with real numbers

Take a graduate three years into work, earning £32,000, with a Plan 5 balance of £48,000. On paper that’s a heavy line: set against £6,000 in savings and a £4,000 car, their net worth is minus £38,000. A frightening figure to a twenty-five-year-old.

Now run it forward. At that salary they repay 9% of the slice above the threshold, a couple of hundred pounds a month, rising as their pay does. Unless their earnings take off, they’ll pay a modest amount each year for forty years and the remaining balance will be written off long before they clear it. That is a lower, flatter income than the typical graduate in the charts above, who nudges their pay up over a career and so repays most of the balance before the clock runs out. The same loan, a different working life, a different amount written off. The £48,000 never becomes a £48,000 bill. It’s the number that makes their net worth look its worst, sitting on a debt engineered to expire.

Compare that with £48,000 of credit-card debt at the same salary. Same minus sign on the balance sheet, completely different reality: the card compounds without mercy, follows you until it’s paid, and reappears every time you apply for credit. Two identical-looking liabilities, two entirely different weights. That gap is exactly what a single net worth figure can’t show you on its own.

Counting it without fearing it

So count the student loan, because net worth only works if you’re honest about both columns. Just don’t let the size of the balance frighten you into treating it like the card. Record it, watch it move, and remember what kind of debt it is: one that shrinks your headline net worth today while setting a ceiling on what it will ever actually cost you. Logging it alongside your other debts and following the trend does more for you than staring at the balance ever will.

The number that looks worst on the page is often the one you understand least, and a student loan is the clearest example of the gap. It’s worth being sure what really counts on each side of the line before you let any single figure tell you how you’re doing.

Last reviewed 6 July 2026.