Sit down to work out your net worth and one number tends to swamp all the others: the value of your home. It’s the biggest line on the page for most UK households, and it’s also the one that starts arguments. Should the place you live count towards your net worth at all? Or is it a figure you can admire but never actually spend?

The question isn’t academic. If you’re measuring your wealth against a target, say a number that clears the mortgage or makes work optional, whether the house counts can shift that target by hundreds of thousands of pounds. Include it and you might look nearly there. Exclude it and the same finances look like a long way off. Same balance sheet, two very different stories.

Here’s the short version, then the nuance. Your home is an asset. Its market value, minus whatever you still owe on the mortgage, is equity, and equity is real wealth by any standard definition. So in the strict accounting sense, yes, it counts. Verdly publishes for education, not financial advice; speak to a regulated adviser for decisions specific to your situation. The interesting part isn’t whether it counts. It’s whether a single net worth figure dominated by your home tells you anything useful.

Why the home looms so large in the UK

Britain has a particular relationship with property, and the data shows it. According to the ONS Wealth and Assets Survey for April 2020 to March 2022, net property wealth made up around 40% of total household wealth in Great Britain, the single largest slice, ahead of private pensions at 35%. Median household wealth over that period was £293,700.

Put those together and the picture is clear. For a typical household the home isn’t one asset among many. It’s close to half the balance sheet. That’s why the include-or-exclude question carries far more weight here than the size of any single savings account ever could. Get the treatment of the house right and the rest of the figure falls into place around it.

The case for leaving it out

The argument against counting your home is more intuitive than it first sounds, and it comes down to one stubborn fact: you have to live somewhere.

Equity locked in the house you sleep in isn’t money you can deploy. You can’t spend a spare bedroom. You can’t move 5% of the kitchen into a pension. To turn that equity into cash you’d have to sell and move somewhere cheaper, rent, or borrow against it, and each of those carries a cost or a catch. The home also produces no income while you live in it. It just sits there, appreciating or not, asking for maintenance and insurance along the way.

There’s a sharper version of this argument for anyone aiming at financial independence. The whole point of a freedom number is the income it can throw off. A £400,000 pension can fund a retirement. A £400,000 house you live in can’t, not without you finding a new roof first. By that logic, counting the home flatters the very number that’s meant to tell you whether you can stop working.

The case for counting it

The trouble with leaving the home out is that the number you’re left with can drift away from reality.

A household with a paid-off £500,000 house and £50,000 in savings is in a materially stronger position than a household with no property and the same £50,000, even though their liquid finances look identical. Ignore the house and you can’t see that difference at all. The equity is real: it can be released by downsizing, unlocked by relocating to a cheaper area, passed on, or borrowed against in later life. It’s illiquid, not imaginary.

The UK tax system underlines the point. When you eventually sell your main home, the gain is generally free of Capital Gains Tax under Private Residence Relief. For most people it’s the single largest pool of wealth they will ever build that the taxman doesn’t touch on the way out. Treating something that valuable, and that tax-favoured, as if it scores zero is its own kind of distortion.

The fix: track two numbers, not one

Most of the heat in this debate comes from forcing one figure to answer two different questions. So don’t.

Track total net worth, with the home included at its current market value minus the outstanding mortgage. That’s your full financial position, the honest measure of everything you’ve built. Then track a second line, liquid (or investable) net worth, which strips the home back out. That’s the part of your wealth that’s actively working for you and that you could reach without selling the roof over your head.

Neither number is the real one. They are two lenses on the same balance sheet. Total net worth answers how wealthy am I, all in. Liquid net worth answers how much have I got that’s doing a job and that I could actually use. Read side by side, they tell you something neither manages alone: not just how big your wealth is, but how much of it you’ve locked into the walls around you.

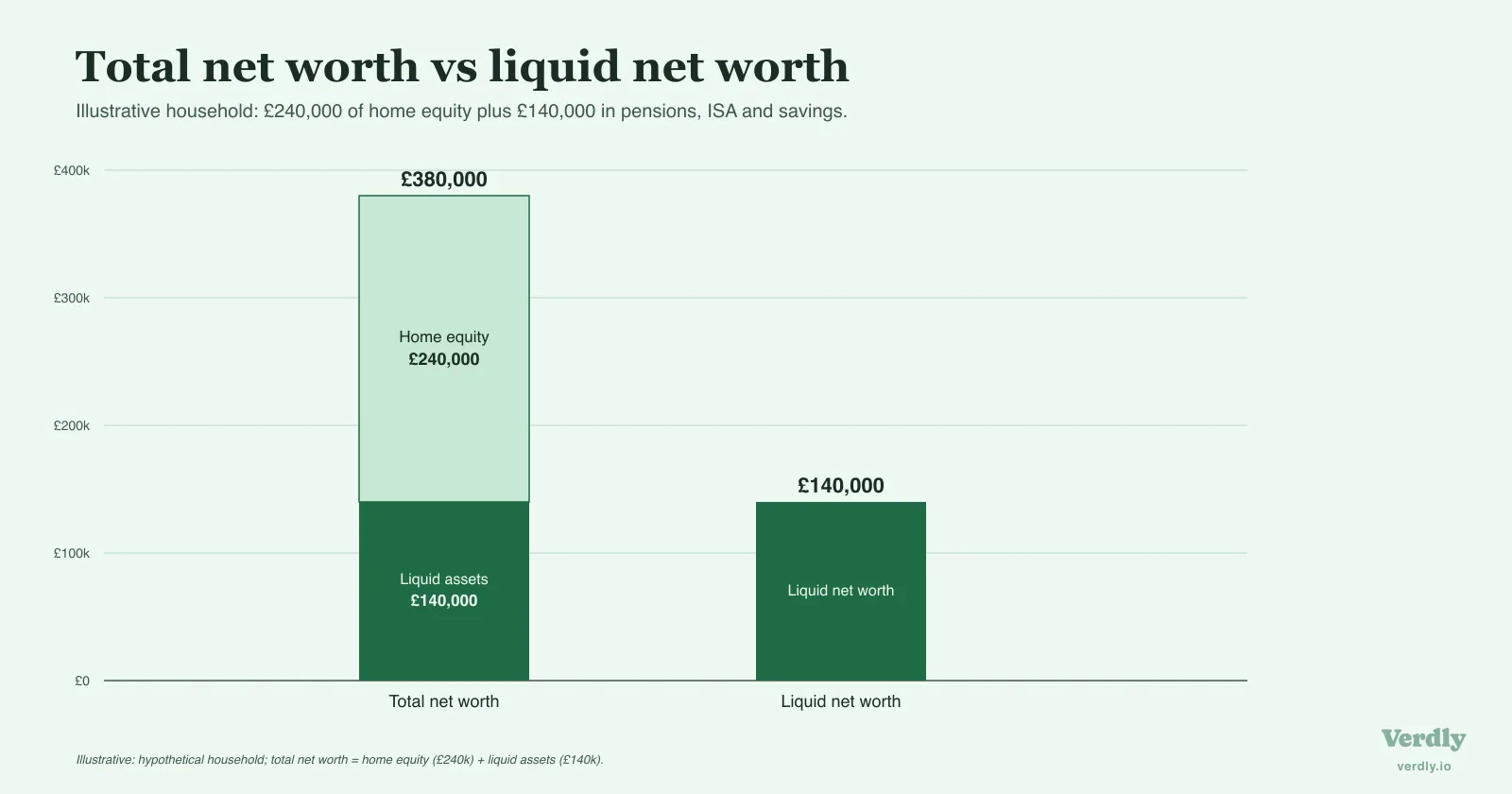

What this looks like with real numbers

Take a couple in their forties. They own a home worth £420,000 with £180,000 left on the mortgage, so £240,000 of equity. Alongside it they hold £35,000 in a Stocks and Shares ISA, £90,000 across two workplace pensions, and £15,000 in easy-access savings. No other debt.

Their total net worth is £380,000: £240,000 of home equity plus £140,000 of everything else. A healthy figure. But close to two-thirds of it is the house.

Their liquid net worth, with the home stripped out, is £140,000. That’s the number that tells them how much of their wealth is invested, accessible, and compounding outside the front door.

Both are true at the same time. Looked at one way, they’re comfortably into six figures and climbing. Looked at the other, the engine of their wealth, the part that can grow into a retirement or a deposit for something else, is a good deal smaller than the headline suggests. A household chasing a target learns far more from watching both lines move than from arguing about which one is allowed to exist.

Comparing yourself to the averages

One practical wrinkle catches people out. The benchmark figures everyone quotes include property. When the ONS reports median household wealth of £293,700, that number has the home baked in. So if you hold your own liquid net worth up against a published average, you’re comparing a figure with the house taken out to one with it left in, and you’ll always come up short. Match like with like. Use total net worth when you’re placing yourself against national figures, and keep liquid net worth for tracking the part of your wealth you can actually steer.

A note on the mortgage

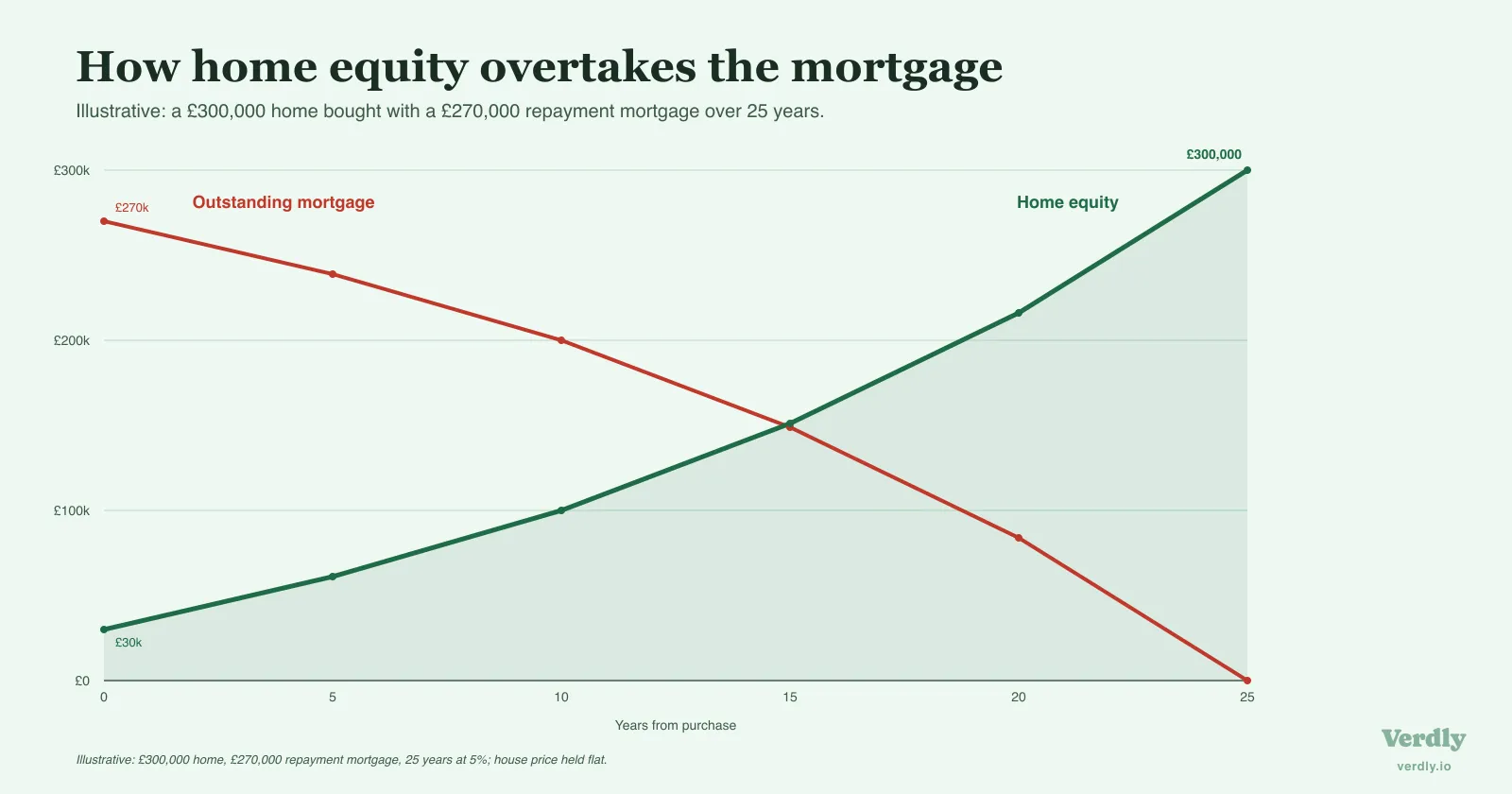

One mistake is worth avoiding: counting the house at full market value while ignoring the loan against it. The asset that belongs in your net worth is the equity, the slice you genuinely own, which is the property’s value minus the outstanding mortgage balance.

In the early years of a repayment mortgage that slice can be thin. Buy at £300,000 with a 10% deposit and, on day one, £270,000 of that house belongs to the bank and £30,000 to you. The equity grows as you pay down the balance and, separately, as the property’s value moves, which is why two people in identical houses can own wildly different amounts of home wealth. Tracking equity rather than headline value keeps the figure honest as the mortgage winds down.

Keeping the home in proportion

The home is rarely the asset that makes or breaks a plan, but it’s almost always the one that makes a single net worth figure hard to read. Keep it in the total, where it belongs, and keep a second line for the wealth you can actually move. The home stops distorting the picture the moment you stop asking one number to carry both meanings.

That’s easier to hold over time than in a single sitting. The value of the house drifts, the mortgage shrinks, the liquid, accessible savings and investments tick along on their own clock, and the relationship between the two lines is the thing actually worth watching. It’s why it helps to track the home as its own line alongside everything else, so the split between what you’ve built and what you can reach stays visible month to month. A single figure is a fact about today. The two of them moving together is the story of where the money is really going.

And the home is only the first asset to spark this argument. A pension you can’t draw on until your late fifties, a car that loses value the moment you drive it, equity tied up in a business: the same question of what truly belongs in the number returns for each of them. The home is simply the one where the stakes, and the price tag, run highest. The fuller answer lives in what counts in your net worth once you look past the front door.

Last reviewed 14 June 2026.